Blockchain is a distributed digital ledger that allows for secure, transparent, and tamper-proof record-keeping. It is the technology that underpins cryptocurrencies like Bitcoin and Ethereum, but it has many other potential use cases. In this blog post, we will explore what blockchain is, how it works and some of its potential applications. We will also look at some of the challenges associated with this technology. By the end of this post, you should have a good understanding of blockchain and its potential implications for the future.

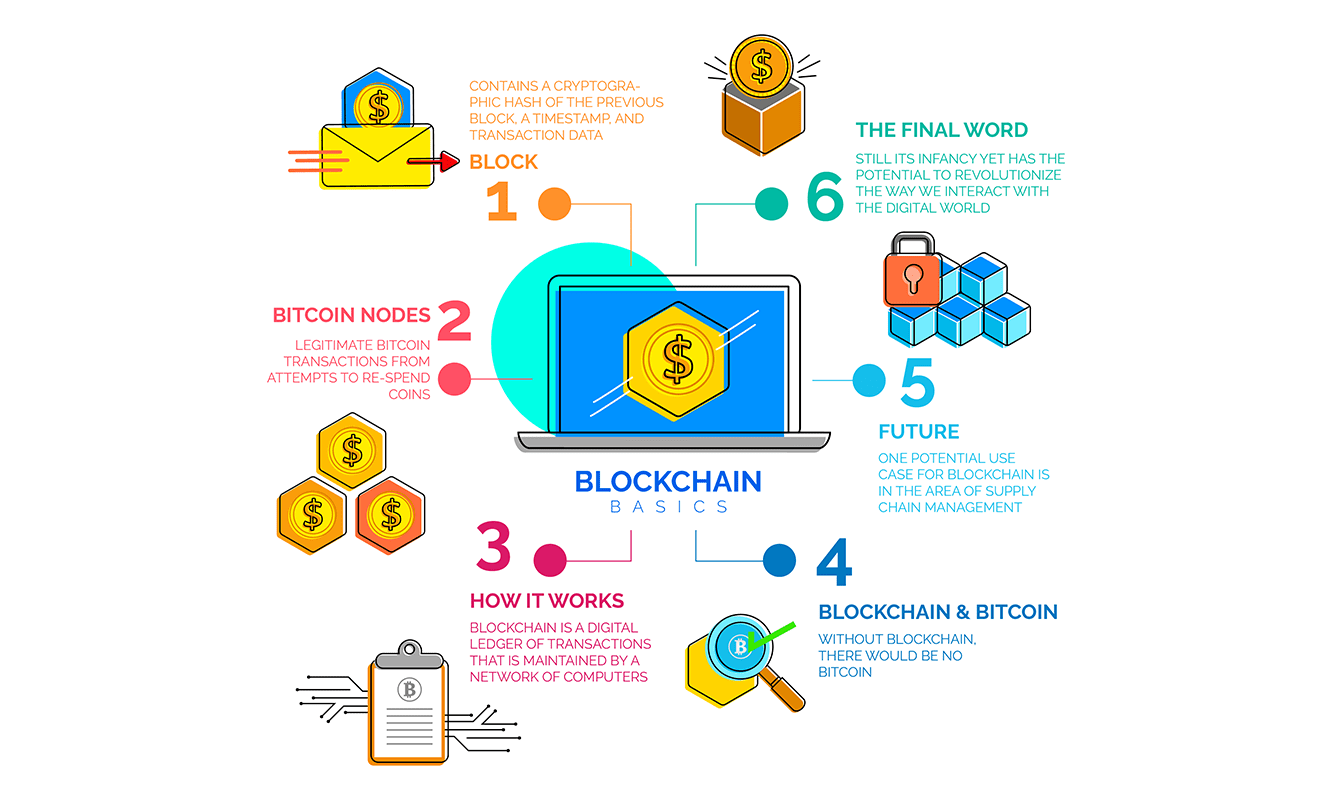

A blockchain is a digital ledger of all cryptocurrency transactions. It is constantly growing as \”completed\” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the blockchain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

The blockchain is an immutable, tamper-proof record of all cryptocurrency transactions. Transactions are bundled into blocks, which are chained together through cryptographic links. This creates a permanent, public record of all transactions that can be verified by anyone.

The key feature of blockchain technology is that it allows for trustless consensus – that is, consensus without the need for a central authority. This means that no single entity can control or manipulate the blockchain. Instead, it is maintained by a distributed network of computers (nodes) running the Bitcoin software.

The key advantage of blockchain technology is that it enables decentralized applications (dapps) to be built on top of it. Dapps are applications that run on a decentralized network and do not require a central point of control or administration. Because they are built on top of the blockchain, dapps are highly resistant to censorship or manipulation by any single entity.

Now that we have a basic understanding of what blockchain technology is, let\’s take a look at how it works. Essentially, a blockchain is a digital ledger of transactions that is maintained by a network of computers. These computers are known as nodes, and they work together to verify and record each transaction that takes place on the network.

Each transaction on the blockchain is encrypted and stored in a block. Once a block is filled with transactions, it is added to the chain and becomes immutable. This means that the data in each block cannot be altered or deleted, which makes the blockchain incredibly secure. In order to change or delete data in a blockchain, an attacker would need to control more than 50% of the network\’s computing power – an unlikely feat.

The fact that blockchain technology is decentralized and secure makes it ideal for use in many industries, including finance, healthcare, government, and more. We\’re only just beginning to scratch the surface of what this groundbreaking technology can do.

The relationship between blockchain and Bitcoin is often misunderstood. Bitcoin is the first and most well-known application of blockchain technology, but it is not the only one. Blockchain is the underlying technology that powers Bitcoin and other cryptocurrencies. Without blockchain, there would be no Bitcoin.

Bitcoin is a decentralized digital currency that uses peer-to-peer (P2P) technology to enable instant payments. Transactions are verified by network nodes through cryptography and recorded in a publicly distributed ledger called a blockchain. Bitcoin was invented by an anonymous person or group of people under the name Satoshi Nakamoto in 2009.

Bitcoins are created as a reward for a process known as mining. They can be exchanged for other currencies, products, and services. As of February 2015, over 100,000 merchants and vendors accepted bitcoin as payment.

The future of blockchain technology is shrouded in potential but fraught with uncertainty. Despite being around for over a decade, blockchain is still in its infancy and has yet to be fully understood or adopted by the mainstream. Nevertheless, there are a number of ways in which blockchain could shape the future, for better or for worse.

One potential use case for blockchain is in the area of supply chain management. The immutable nature of blockchain could help to streamline supply chains and make them more efficient. This would have a knock-on effect on the prices of goods and services, as well as on the environment, as fewer resources would be required to produce and transport them.

Another possible use case for blockchain is in the realm of identity management. Blockchain could provide a secure and tamper-proof way to store personal data and information. This would have far-reaching implications for both individuals and businesses, who would no longer need to worry about their data being hacked or leaked.

Of course, these are just two potential use cases for blockchain technology. It remains to be seen what other uses will be found for this groundbreaking technology in the years to come.

Blockchain technology is still in its infancy, but it has the potential to revolutionize the way we interact with the digital world. For now, it\’s important to understand the basics of how blockchain works and what it could mean for the future.